Encumbrance Certificate Explained in 7 Points for Home Buyers

Adv(Col) Raj Kumar

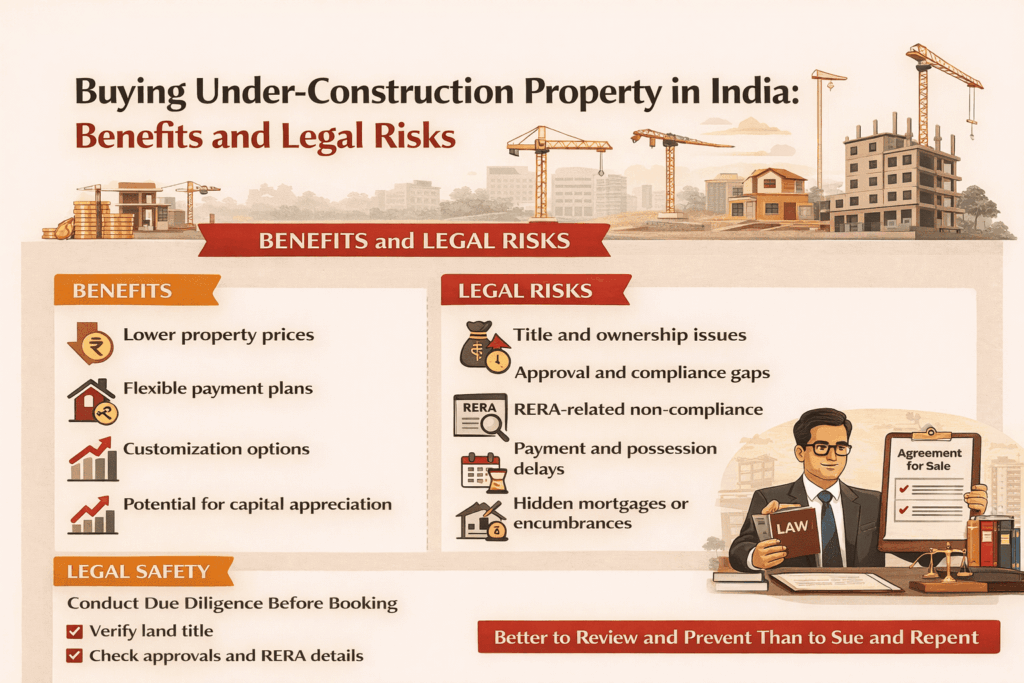

When buying a house or flat in India, most home buyers focus on ownership documents and price negotiations. One crucial document that is often misunderstood or overlooked is the Encumbrance Certificate (EC). An EC plays a vital role in confirming whether a property is free from legal and financial liabilities.

Understanding what an Encumbrance Certificate shows, and what it does not, can help home buyers avoid disputes, hidden loans, and costly litigation. This article explains in 7 points all about EC.

1. What Is an Encumbrance Certificate?

An Encumbrance Certificate is an official document issued by the Sub-Registrar’s Office that reflects all registered transactions related to a property during a specified period.

It records details such as:

• Sale deeds

• Mortgages registered with banks or lenders

• Gift deeds, partition deeds, or release deeds

If no transactions are registered during the chosen period, the EC will state that the property is free from registered encumbrances.

2. Why the Encumbrance Certificate Is Important for Home Buyers

The primary purpose of an Encumbrance Certificate is to confirm whether the property has:

• An existing loan or mortgage

• A registered charge in favour of a bank or financial institution

• Prior sale or transfer affecting ownership

For home buyers, this document helps verify that the seller is not transferring a property that is already burdened with legal or financial obligations.

Banks also rely on the Encumbrance Certificate while processing home loan applications, making it an essential part of legal due diligence.

3. What an Encumbrance Certificate Shows—and What It Does Not

An Encumbrance Certificate reflects only registered transactions. This distinction is critical.

It shows:

• Registered mortgages

• Registered sales or transfers

• Registered court attachments

It does not show:

• Unregistered agreements

• Pending lawsuits not recorded as attachments/final judgments

• Family or inheritance disputes

• Oral arrangements or informal loans

Therefore, while an EC is necessary, it is not sufficient by itself to confirm that a property is completely risk-free.

4. How Home Buyers Typically Misunderstand the EC

Many buyers assume that a “Nil Encumbrance” certificate guarantees a clear property title. This is a misconception.

A Nil EC only confirms that no registered encumbrances exist during the selected period. It does not guarantee:

• Clear ownership

• Absence of pending litigation

• Valid land use or building approvals

This is why an Encumbrance Certificate must always be read alongwith the title documents and other approvals.

5. How to Apply for an Encumbrance Certificate

Home buyers can apply for an EC:

• Online through state land registration portals (e.g. Kaveri portal in Karnataka)

• Offline at the Sub-Registrar’s Office

The applicant must specify:

• Property details

• Time period for which the EC is required

6. Is an Encumbrance Certificate Mandatory?

While there is no single law mandating an EC for all purchases, it is practically indispensable.

An EC is required for:

• Home loan approval

• Legal due diligence

• Confirming absence of registered loans or charges

Proceeding without an EC significantly increases legal risk for homebuyers.

7. Practical Points for Home Buyers

Home buyers should:

• Obtain an EC for an extended period and not just the latest one

• Match EC entries with title documents

• Verify closure of any past mortgages

• Avoid relying on EC alone

Understanding how the EC fits into the overall purchase process is easier when read alongside our guide on Home Buying in India.

Conclusion

An Encumbrance Certificate is a critical risk-assessment document for home buyers, but it is not a standalone guarantee of safety. It confirms the absence or presence of registered liabilities—not overall legal compliance. For buyers, the safest approach is to treat the Encumbrance Certificate as one part of a comprehensive legal due diligence process.

Disclaimer: This article is for informational purposes only and does not constitute legal advice. Professional consultation is recommended for individual cases.